What does your journey toward homeownership entail?

Embarking on a new chapter of living and working in Canada can be an exhilarating but potentially daunting experience. If you’re considering purchasing a home, we’re here to provide expert mortgage guidance (in your language of choice) and secure the most favourable rates to maximize your savings.

Newcomer to Canada? Simplifying Your Mortgage Journey.

Have aspirations of homeownership in Canada? Our approachable and highly skilled mortgage brokers are here to guide you every step of the way.

Where are you arriving from? We’re fluent in the universal language of mortgages, thanks to our diverse team of brokers who speak multiple languages. This ensures you have a clear understanding of your mortgage process.

We’re also genuinely committed to your best interests because we’re real people who have chosen Canada as our home too. Whether you are from any corner of the world, we extend a warm welcome to our wonderful nation.

Is it possible to secure a mortgage as a newcomer in Canada?

As a newcomer, there are specific qualifications and eligibility criteria you’ll need to satisfy to purchase a primary residence in Canada. These include:

- Holding a valid work permit and having permission to work in Canada (additional conditions may apply).

- Possessing permanent resident status.

- Being a refugee or temporary worker (additional conditions may apply).

Path to Homeownership:

Mortgages Tailored for PR Cardholders, Work Visa and Refugees

Understanding Mortgages in Canada

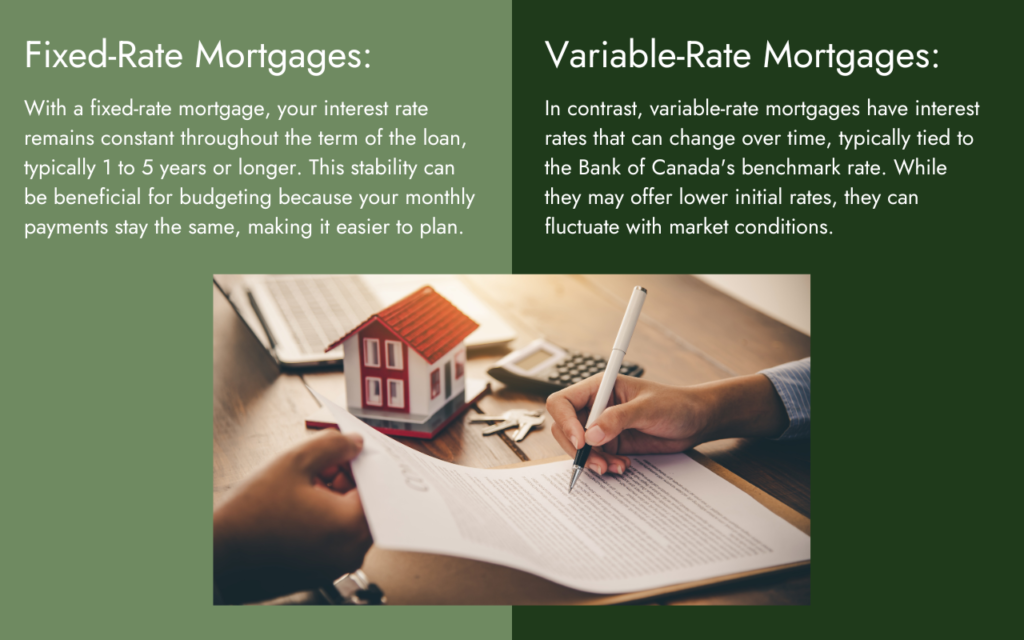

Let’s start with the basics. A mortgage is a loan you take out to buy a home. In Canada, mortgages are offered by banks, credit unions, and other financial institutions. They come in various types, including fixed-rate and variable-rate mortgages.

What Do Mortgage Terms Mean?

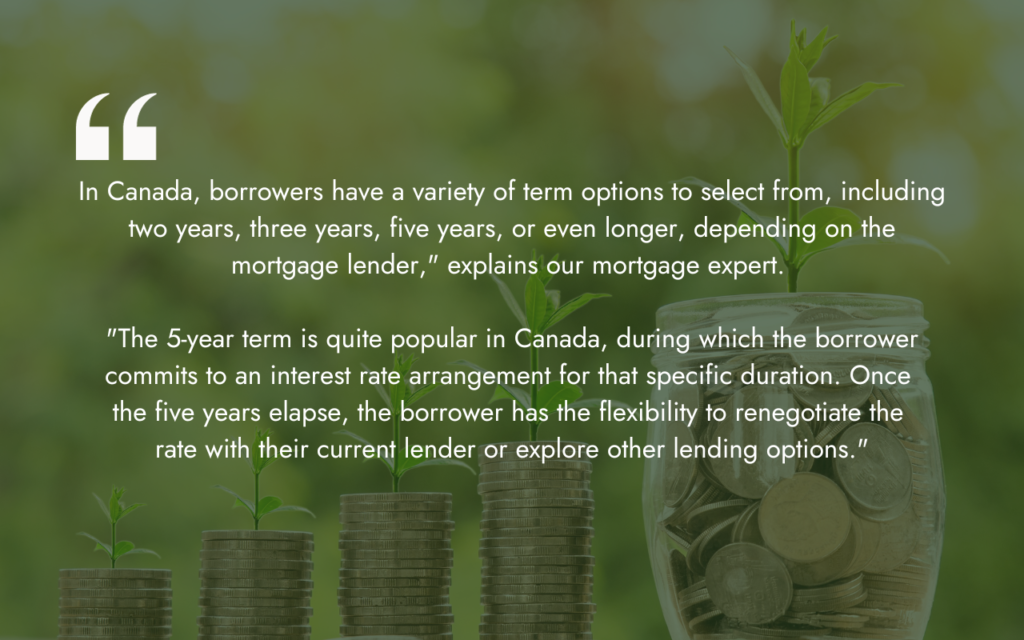

A mortgage term signifies the duration during which the terms of your mortgage, including the interest rate, monthly payment, and other conditions, remain fixed. Once the term concludes, the mortgage becomes due and payable unless you choose to renew it. It’s important to note that the term’s length is typically shorter than the mortgage’s amortization period, which represents the total time required to repay the entire mortgage balance. For instance, you might opt for a 5-year mortgage term with a 25-year amortization period.

A mortgage term can be closed or open. With a closed term, if you decide to repay the mortgage before the end of the term, a prepayment charge may apply. With an open term, you can generally repay the mortgage at any time during the term without a prepayment charge. ”That’s why it’s important to make sure you choose the right term for you.”

A mortgage term can be closed or open. With a closed term, if you decide to repay the mortgage before the end of the term, a prepayment charge may apply. With an open term, you can generally repay the mortgage at any time during the term without a prepayment charge. ”That’s why it’s important to make sure you choose the right term for you.”

Understanding the Amortization Period

In certain countries, the terms ‘amortization period’ and ‘loan term’ are used interchangeably. However, in Canada, they often differ. The amortization period refers to the duration it will take you to fully repay your entire mortgage debt, including accrued interest, based on regular payments at a predetermined interest rate.

”Typical amortization periods in Canada are 10, 20, and 25 years.”

When you opt for a longer amortization period, your monthly payments are lower, but you’ll pay more interest over the life of your loan due to the extended borrowing duration. Conversely, choosing a shorter amortization period results in higher monthly payments but less interest paid over the loan’s lifetime, as you’ll clear the debt more quickly.

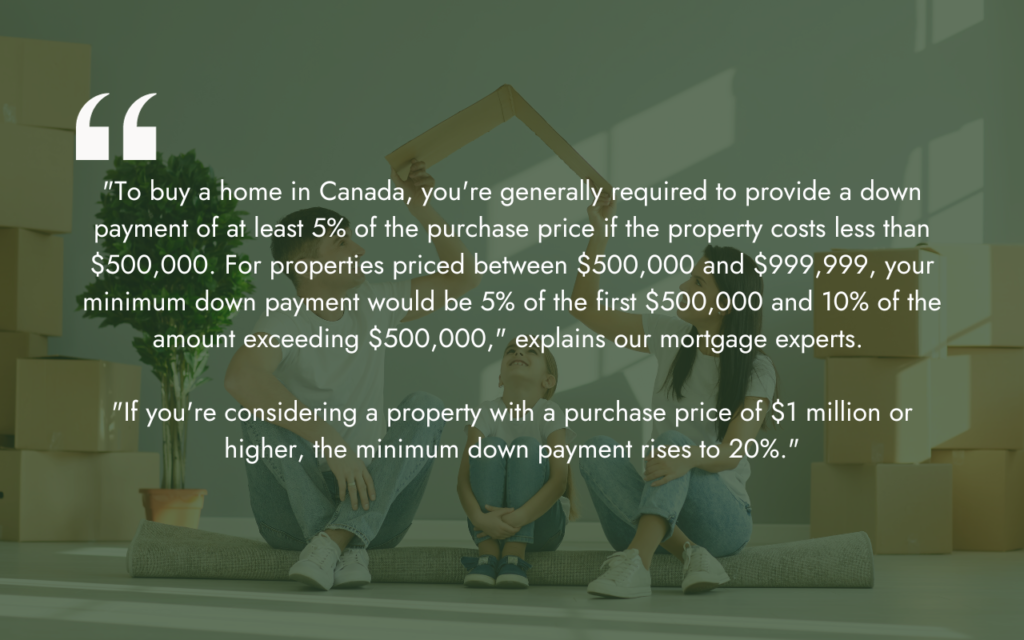

Canadian Mortgages and Down Payments

When it comes to purchasing a home in Canada, a down payment is a crucial component that complements your mortgage, making homeownership possible.

If your down payment is less than 20% of the purchase price, you can still secure a mortgage, but you’ll be required to obtain mortgage default insurance. This insurance applies to homes valued at less than $1 million and typically ranges from 2.80% to 4.00% of your mortgage loan, depending on the amount you’re borrowing and the size of your down payment.

The reassuring aspect is that applying for mortgage default insurance isn’t an additional step you need to take. Mortgage lenders automatically handle this on your behalf and will either present it to you as a lump-sum fee or incorporate it into your mortgage balance.

Insured Mortgage Programs Tailored for Newcomers in Canada

Canada offers specialized insured mortgage programs designed to assist newcomers to the country in realizing their homeownership dreams. These programs are offered by all three mortgage default insurance companies: CMHC, Sagen, and Canada Guaranty.

Key Features of Newcomer Mortgage Programs Newcomers who hold permanent resident status gain access to a comprehensive range of mortgage insurance products from CMHC, Sagen, and Canada Guaranty, provided they meet the specific eligibility requirements for each product.

For permanent residents who have limited Canadian credit history and lack access to foreign credit bureaus, alternative payment history sources may be considered for Loan-to-Value (LTV) ratios of up to 95%.

Newcomers with non-permanent resident status must adhere to federal eligibility criteria. They may be eligible for insured financing with an LTV ratio of up to 90% for the acquisition of a single-unit, owner-occupied residential property.

It’s important to note that residency status doesn’t result in additional fees or premiums; the standard product-specific premiums apply across the board.

The process of applying for a mortgage in Canada involves several steps:

The Home Buyers’ Plan (HBP) allows you to withdraw funds from your Registered Retirement Savings Plan (RRSP) to buy or build a qualifying home.

Conclusion

Owning a home in Canada is an achievable dream for newcomers. By understanding the mortgage process, building your credit history, and working with experienced professionals, you can embark on your homeownership journey with confidence. Remember, you’re not alone in this endeavour. Many have walked this path before you and have found success in making Canada their cherished home.

If you have any questions or need personalized guidance, please don’t hesitate to reach out to our team of experts. We’re here to help you turn your dream of homeownership in Canada into a reality.

Welcome to Canada, and welcome to the world of homeownership!